How to Invest for Beginners: Basics of Investing in 2025

As a financial therapist, I’m known for getting into the money feels. But today we’re doing things a little different. This is all about the numbers and how to invest for beginners.

Of course, we’ll touch on money mindset because, though not many people will admit this, investing is emotional.

Before we get really into it, I want you to know two things:

- I do have a completely FREE guide on How to Invest for Beginners. So, of course, take a look at that!

- This is not financial advice. I am not a financial advisor. This is for educational purposes.

I want you to understand how to think about investing and how the numbers can shape up for you and improve your life.

Alright, now that my lawyer is happy, we can get to the good stuff.

You can listen to the full How to Invest for Beginners episode on Financial Self-Care with Financial Therapist, Lindsey here on Spotify or Apple Podcasts.

How to Invest for Beginners: Saving vs. Investing

I want to start by differentiating saving and investing. Most of us have heard the saying, “Save for a rainy day.”

But the question is: Can you really save your way to wealth?

Unfortunately, the answer is a resounding, “No.“

There are two main reasons why: Inflation and Compounding Interest

Inflation

We’ll start by talking about inflation.

Inflation has been a HUGE topic of conversation, and I want to break it down in very simplistic terms here.

If you keep $10,000 cash under the mattress or – if you’re not 100-years-old – in a savings account for 20 years, you’ll still have $10,000 in 20 years. The problem is, the purchasing power of that money will have gone way down.

Have you ever heard a really old person say (old person voice), “Well in my day we could walk up to the gas station and get a piece of candy for five cents?”

Sure, grandpa, but five cents isn’t what it used to be because purchasing power has changed.

Here’s an example:

Do you remember how, in early 2023, everyone freaked out about the price of eggs?

That was because inflation was at an incredibly high 8.8%. A dozen eggs went from costing $2.00 in the beginning of 2022 to $3.40 a year later.

And that’s just eggs. Most other prices dramatically increased, too.

Lucky for us, inflation percentages ebb and flow, and the average rate of inflation is about 3%.

Inflation Example

To use a real life example:

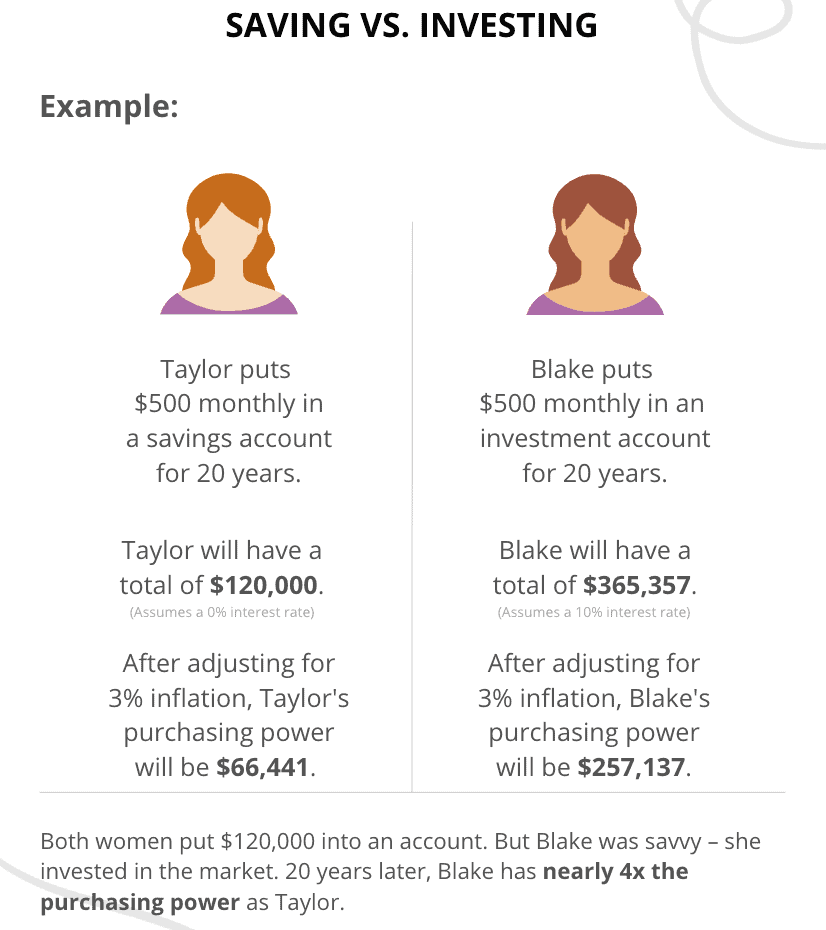

We have two friends, Taylor and Blake.

Taylor puts $500 under her mattress every month for 20 years (Taylor learned everything she knows from her grandma, so mattress money was the obvious choice).

After 20 years has come and gone, Taylor will have $120,000 under her mattress. BUT after adjusting for 3% average rate of inflation, Taylor’s purchasing power – AKA that money will only be worth – $66,441.

Blake, on the other hand, puts $500 per month for 20 years in an investment account (She learned everything she knows from her favorite financial therapist, Lindsey, so investing was the obvious choice.)

Using a 10% rate of return on that money, Blake will have $365,357. However, we also need to adjust for inflation. And using that average 3% number, Blake’s purchasing power of her money is $257,137 in today’s dollar value.

Do you see what happened here?

Both women put aside $120,000 over 20 years, but Taylor ended with just over $66,000 and Blake had well over $250,000. Blake was savvy; she invested in the market for the long-term. Now, Blake has nearly 4x the purchasing power has Taylor.

Saving for a rainy day doesn’t work because of inflation.

But you might be thinking: “How on earth did Blake turn $120,000 into over $257,000?” And the answer is compounding interest.

Compounding Interest

This is where I would cue the music *do you believe in magic* because compounding interest truly is enchanting.

Compounding interest is the earnings you gain on both the principal balance (what you put into an investing account) and the interest you earn on the total balance.

So, say you put $500 into an investment account this month and you earn 10% interest on that money. Next month, you put another $500 in that investment account, but you earned $3.99 last month.

The interest is compounding, not just on your own $1,000 that you’ve contributed, but on the additional $3.99 you earned in month one. At the end of month two, you earned $8.01.

Then, in month three, you earn $12.06 in interest in addition to the $1,500 you’ve now put in the account.

Month 4: $16.14.

Month 5: $20.26.

Month 6: $24.40.

After 6 months, you’ve earned $60.45 in interest.

$60.45 is not life-changing money, but do this for 30 years, and it will be.

You, personally, will have contributed $180,000 to your investment account. But you will have earned a lifetime total of $851,421.66. Making the total in your investment account $1,031,421.66.

That is life-changing money.

Compounding interest is magical, but to feed it, you need time.

There is one thing I want to note here and that is how we decide what number to use for your rate of return (or the money you’re earning in interest).

The S&P 500 has averaged about 10% over the last 50 years.

Technically, it’s 11.47%, but I like to use conservative numbers because I would rather error on the low side and be pleasantly surprised with more money than error on the high side and be unpleasantly surprised by less money.

Assume 10% is the average rate of return. BUT remember, the average rate of inflation is 3%. So we generally use 7% as the average compounding interest rate.

10% average rate of return minus 3% inflation equals 7%.

I told you this post would be a little more numbers heavy, but stick with me.

Again, you can grab my FREE Investing for Beginners guide that has infographics and this all laid out in written form for my visual learners out there.

Compounding Interest Example

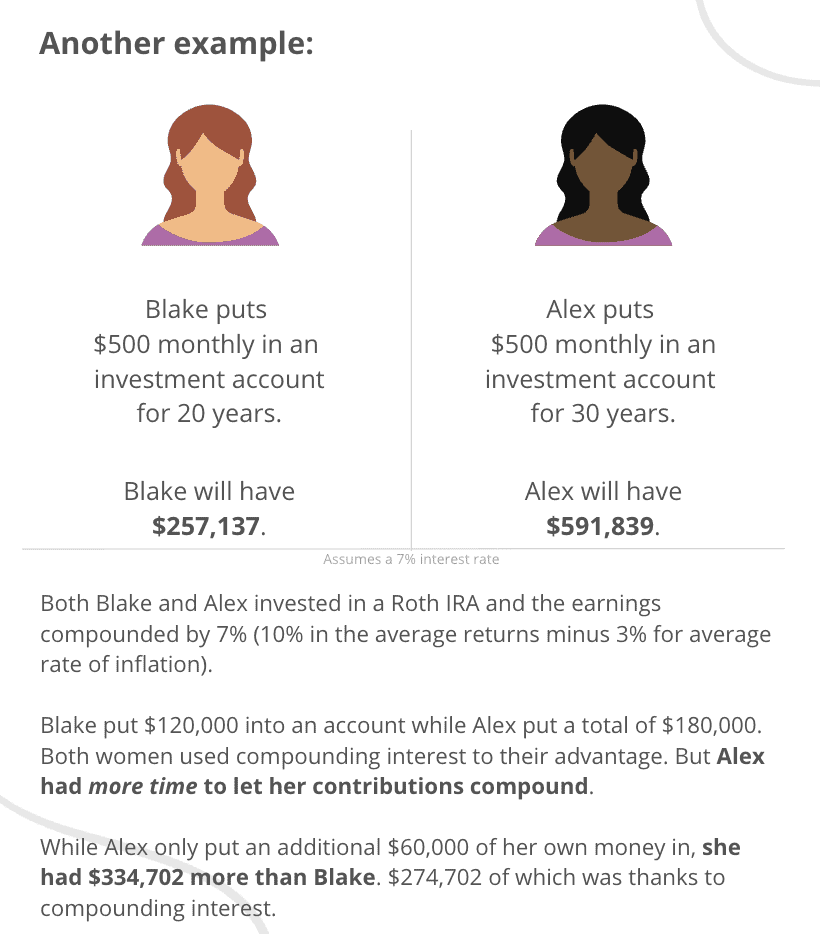

Going back to our girl Blake from our first example. If you remember, she put $500 into her investment account every month for 20 years. And using that 7% rate of return, Blake will have $257,137. She contributed $120,000 of her own money to that account. And she earned more than $137,000 in compounding interest.

And we have a new friend on the block. Her name is Alex.

Alex put $500 into her investment account every month for 30 years. She will have $591,839 total. Alex only contributed $180,000 of her own money, so only $60,000 more than Blake did, but she earned almost $412,000 of interest, nearly $275,000 more than Blake did.

This is why TIME is your most important resource for investing and why you can’t keep putting it off.

Saving vs. Investing Takeaways

What are the key takeaways here?

- Saving your way to wealth is simply not possible. You have to consider how inflation impacts purchasing power.

- The more time you have in the market, the better. More time means more opportunity for compounding interest to do it’s thing!

- The average rate of inflation is approx. 3%.

- Investing in a strategic index fund can average a rate of return of 10%.

- When doing your own calculations (with the funds you have available to invest) on a compound investment calculator, you should use an assumed 7% interest rate.

So those are the very basic concepts and foundations of investing. Which are really important and I hope I’ve convinced you to want to invest.

How to Invest for Beginners: Where to Invest Your Money

And the next step is figuring out where to invest your money.

In this next part, we’re discussing Roth IRAs, employer sponsored plans like a 401(k) and 403(b), health savings accounts, child education plans or custodial accounts, and brokerage accounts.

Roth IRAs

Let’s start with Roth IRAs.

IRA stands for Individual Retirement Account. Unlike a pension, 401(k) or 403(b) plan, a Roth IRA isn’t sponsored by an employer. Rather, it’s individually owned by you.

The Roth IRA is one of my favorite accounts because it is very accessible, meaning most Americans can contribute to a Roth IRA and it is a tax advantaged account.

Roth IRAs: Basic Facts

These are some things to know about your Roth IRA.

First, is the 5-Year Rule. The five year rule applies to the Roth IRA and it means after being vested for five years –so after you have had the account for 5 years – you can access your contributions anytime without penalty.

This is a common misconception with retirement accounts.

Most people think they are locked in some crazy vault until you retire. Which is partially true.

But the reality is, you can access your contributions, again the money you’ve contributed, after 5-years.

Even though you CAN access your contributions, you shouldn’t. As we talked about in the beginning of this episode, your investments are better left untouched for decades, like our girl Alex.

Next, you can withdraw earnings from your Roth IRA when you turn 59 and a half. Weird, I know, but this is the vault part.

Contributions and earnings are different. Contributions are what you put in. Earnings are the magical compounding interest we already talked about. You cannot access your earnings without penalty until you’re 59 and a half.

The next thing to know about a Roth IRA is you put taxed money into a Roth IRA. Don’t let this trip you up. Taxed money is just fancy lingo for any money that is already in your checking account. That’s what you can transfer or deposit into a Roth IRA.

As I said before, the Roth IRA is a tax-advantaged account. You have already been taxed on the money in your checking account.

But when you contribute to a Roth IRA, your earnings grow tax-free, which is a HUGE advantage.

Your withdrawals, so when you’re 59-and-a-half or older and take money out of your Roth IRA, are also tax-free! This is why we LOVE the Roth IRA. Not paying taxes on this money means more money in your pocket.

And finally, the last thing I want you to know about Roth IRAs (and some other investment accounts) is that it’s really just that, an account.

Meaning, once you open a Roth IRA, you need to actually invest the money. Otherwise, it’s just chillin’ like a basic checking account. Don’t worry, we’ll talk about how to do this, too.

Like I said before, I love Roth IRAs because of the accessibility of then, but there are some limitations to this type of investment account.

Roth IRAs: Income Limits

The first is, there are income limits. Meaning if you make too much money, you cannot contribute to a Roth IRA. For single tax filers in 2025, the income limit is $150,000 per year. For those married, filing jointly, the income limit is $236,000.

Roth IRAs: Contribution Limits

There are contribution limits, meaning you can only put so much into this investment account per year.

As of 2025, the contribution limits are $7,000 if you’re under the age of 50 (which breaks down to $583 per month) or $8,000 if you’re 50 years of age or older.

The reason these limits exist is because of the tax advantages. It’s almost a too-good-to-be-true account, so they limit how much you’re able to put into it.

Okay, so that’s the first account. And a mighty-fine one at that. But let’s talk about your other options!

Employer Sponsored Plans: 401(k) or 403(b)

Employer sponsored plans are things like 401(k)s and 403(b)s. Depending on where you work, you may have the opportunity to invest through an employer sponsored plan.

Unlike a Roth IRA, you can’t touch ANY of these funds (contributions or earnings) until you are 59-and-a-half without penalty. So again, think of investing in these accounts as a locked vault.

Opposite from the Roth IRA, initial contributions to a 401(k) or a 403(b) are NOT taxed. Instead, you’re taxed on this money when you withdraw it.

So, it’s still a tax advantaged account, but the taxes are taken later in life.

401(k) vs. 403(b)

The two biggest differences between a 401(k) and a 403(b) are 401(k)s are generally offered by for-profit companies and 403(b)s are generally offered by tax-exempt organizations.

Companies offering a 401(k) usually offer some sort of matching program versus very few 403(b) organizations offering a match.

Employer Sponsored Plans: Contribution Limits

There are contribution limits to these employer sponsored plans. In 2025, you can individually contribute $23,500 per year to your 401(k) or 403(b). And that does NOT include your employer’s match.

This is why you should ALWAYS be contributing to your 401(k) or 403(b), up to your employer’s match program. Otherwise you are leaving “free” money on the table.

If you have more questions about your 401(k) or 403(b), you can contact your HR representative at your work!

That’s the basics of employer sponsored plans.

Health Savings Accounts

Next up, we have a Health Savings Accounts also known as an HSA, not to be confused with a Flexible Spending Account also referred to as an FSA.

Many people don’t know this, but with an HSA, you actually can invest this money.

And when I say many people don’t know this, I mean it.

I was talking to my previous financial advisor, someone who invests in the stock market for a living, and HE did not even know that you could invest your HSA funds. Don’t worry, I’ve since fired him.

Let me tell you, I LOVE an HSA. Because the HSA is the best kept investing secret due to it’s triple tax advantage.

This means, with an HSA, you are NOT taxed on contributions, earnings, or withdrawals. This money is NEVER taxed!

And a commonly asked question is: If the HSA is such a bargain investing tool, why do you mostly talk about Roth IRAs. And it’s a great question.

The answer is simple: Lack of access.

Only about 10% of Americans even qualify for an HSA. And of that 10% far less actually use it as an investing tool.

In order to have access to an HSA, it requires a high-deductible healthcare plan, which makes it challenging to use as an investment tool if you experience frequent medical interventions.

However, if you are one of the lucky one that does have access to an HSA, it might be time to take advantage of this investing account.

Health Savings Account: The Benefits

There are a ton of benefits to having an HSA.

There are no income limits for contributing to an HSA. You could be a gazillionaire and still have an HSA.

You can withdraw funds from your HSA at any time to pay for qualifying medical expenses. Qualified medical expenses are things like chiropractor visits or x-rays or crutches.

I’ve linked an entire pdf about what you can and can’t pay for with an HSA in the show notes.

Our family is using our HSA as a retirement vehicle. But in the event that we have a serious medical expense, we can withdraw funds (again, tax-free) whenever we need to.

You don’t have to use your HSA funds. Unlike a flex spending account, which is use-it-or-lose-it.

And finally, when you turn 65, you can withdraw HSA funds for any purpose without penalty.

Though, as an additional note, if you do this, you’ll owe taxes on the withdrawal at your income tax rate, making the HSA a double tax-advantaged account. Which is still great, just a little less magical.

Though there are no income limits to an HSA, there are contribution limits.

In 2025, you can contribute $4,300 for self-only coverage, and $8,550 for family coverage. And again, in 2025, if you’re over the age of 55, you can add $1,000 to those figures.

Like the employer sponsored plans, you can always contact your HR rep for more help with your HSA contributions.

Child Accounts

Moving on to Child accounts. And, mama, it’s time to have a heart-to-heart. I know you want what’s best for your baby.

But I promise, first, you must set yourself up for success.

You have to invest for yourself in something like a 401(k) or Roth IRA and make sure YOU are set up for success in your own retirement before contributing to your kids financial future.

Then, and only then, if there are funds left over, you can contribute to your baby’s accounts.

You don’t want to spend all your efforts on setting your kid up for success, just to need their financial help later in life.

The absolute best thing you can do for your babies is educate them about personal finance. Education does not mean giving them money. Giving them money is a nice bonus, buy only if you can afford it and only if you teach them HOW to use that money well.

You need to be practicing financial self-care for yourself – model that for your children. That’s the best advantage you can give your kids.

With that said, I want you to be aware of your options for investing in child accounts. Those options include: Education Plans and Custodial Accounts.

You can read more about Education Plans and Custodial Accounts in my FREE How to Invest for Beginners guide here.

Brokerage Account

The final investment account we will talk about today is a brokerage account.

A brokerage account is basically a fancy word for a regular ‘ol investment account.

You can open a brokerage account quickly and easily. And there aren’t a whole lot of stipulations. Meaning, there are no income limits or contribution limits. It’s undoubtedly the most accessible account.

The downside of a brokerage account is there are no tax advantages.

That’s partially why I push for investing in retirement accounts first. The tax advantages of Roth IRAs, HSAs, 401(k)s, etc. make your hard-earned money go further.

And finally, because of how easily accessible they are, brokerage accounts can tempt a person into trying to “play” the market. That’s a big no-go for me. I like to invest it and forget it. I don’t day-trade or play the market at all.

Personally, we have one brokerage account and use it for a small percentage of our overall portfolio. It has a little money invested in a riskier allocation. Which I will talk about more next.

There are other types of investment accounts like a SEP IRA, Simple IRA, Back Door IRA, and more. But this episode is called Investing for Beginners, and I’ve probably already overwhelmed you with your options.

I’ll be interviewing Madison Sharick from Madi Manages Money who is a fee-only financial advisor. And we will be going in-depth about other accounts and secrets of AUM fund managers in that episode.

How to Invest for Beginners: How to Invest Your Money

Okay, how to invest your money.

We’ve covered what investing is and what type of accounts you can open. Now it’s time to talk about how to invest your money.

All of the accounts we’ve talked about – Roth IRAs, employer sponsored accounts, HSAs, and brokerage accounts – are simply that: an account. In order to actually invest, you need to buy stocks and bonds.

This is the part where people get really intimidated. I hear things like: “I don’t know anything about the stock market!” and “Isn’t investing just gambling?” Or simply, “I’m scared.”

Look, you’ve made it this far. You should be proud of that. Don’t let this part scare you away from having the financial independence you want.

Stocks vs. Bonds

First and foremost you need to know the difference between stocks and bonds.

Typically, financial experts recommend you have a diversified portfolio, meaning you own both stocks and bonds.

Stocks because they’re riskier but potentially have a greater return on investment. Bonds because they’re less risky, but still give you returns.

I don’t want to get too technical with this, so I’m going to give you the very basic overview.

Stocks

A stock, also known as equity, represents a share or partial ownership of a public company. Common examples are buying shares of Amazon or Apple.

All stocks have a ticker symbol or letters that represents a unique company. Amazon’s ticker is AMZN and Apple’s ticker is AAPL.

I don’t buy individual stocks because they can be quite volatile; there is more risk involved. As we keep going, you’ll learn what I do, instead.

Bonds

Bonds, on the other hand, don’t give you ownership of a company. Rather, with bonds, you’re essentially giving an agency a loan and they’ll pay you back with interest.

A bond is usually issued through governments and corporations. And bonds are far less risky than stocks.

Mutual Funds

Now there are things called Mutual Funds. And mutual funds are basically a basket of different stocks. They’re chosen and actively managed by a credentialed investor often called a fund manager.

If you go to a financial advisor and say, “Here’s $1,000. Can you invest that for me?” They are going to ask you some questions about your financial goals and your comfortability with risk. Then, they go and hand-pick stocks and bonds for you.

For doing this, they charge a fee, sometimes called an expense ratio.

Essentially, because they are actively managing your funds, the credential investors take a percentage of your earnings. This is called Assets under management or AUM. A fund manager generally charges 1%-2% for an AUM.

One or even two percent doesn’t sound like a lot, but I’ll give you an example of how much it actually impacts your wealth after we discuss index funds.

Index Funds

Index funds are just the smarter mutual fund. Essentially, index funds are the same thing as a mutual fund, a basket of different investments.

But rather than being actively chosen and managed by a credentialed investor, an index fund is passively managed through a professional financial firm.

As opposed to the exorbitant 1%-2% fees of a mutual fund, index funds generally charge about a .25% or a .5% fee.

Remember that $1,000 you were going to take to a credentialed investor? Instead, you can open an account with a Robo-Advisor (Fidelity like Vanguard). And pick a pre-made basket of stocks.

Mutual Funds vs. Index Funds

You can kind of think of this like apples. Stocks are pink lady red apples. Bonds are granny smith green apples. When you go to the store, you can just buy a basket of apples. Those are the mutual funds or index funds.

Earlier in this post, I talked about firing my financial advisor. And one reason was because he didn’t know that you could invest your HSA funds, sure.

But the MAIN reason I fired him was due to the insane fees he was charging me.

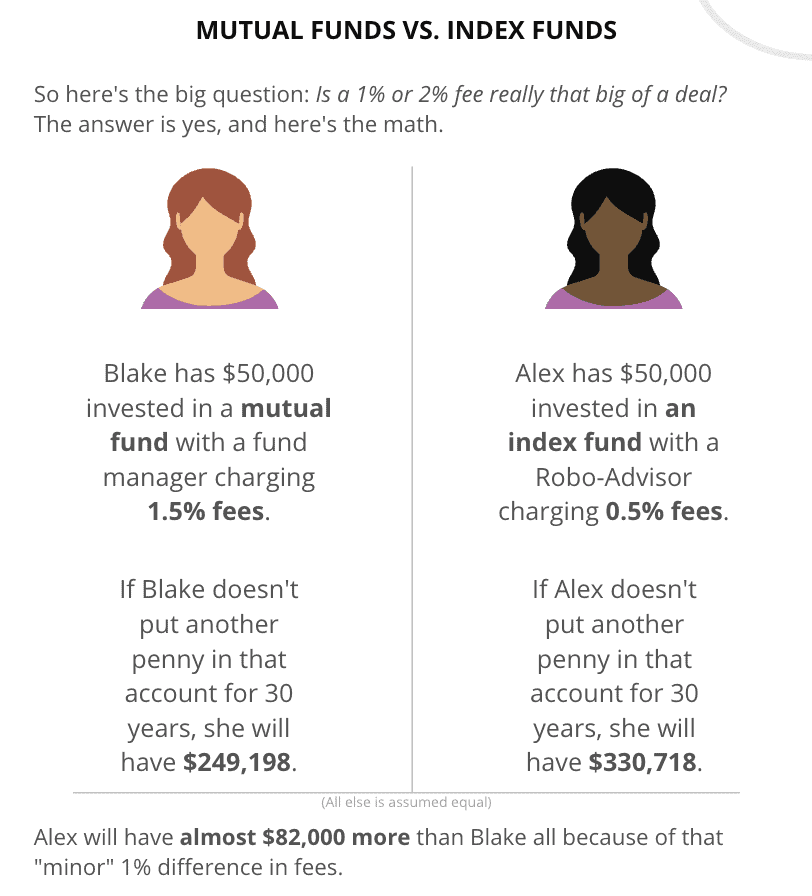

The big question is: Is a 1% or 2% fee really that big of a deal?

The answer is yes, and here’s the math.

Mutual Funds vs. Index Funds Example

Blake, our girl who is trying. She’s trying really hard to do the right thing. And she has $50,000 invested in a mutual fund with a fund manager charging 1.5% fees – this is the same fee my financial advisor was charging me.

If Blake doesn’t put another penny into that account for 30 years, she will have $249,198.

Now, our savvy girl Alex is back. Alex has $50,000 invested in an index funds with a .5% fee (which is still generally high for an index fund, but we’ll keep it on the high end for this example).

If Alex doesn’t put another penny in that account for 30 years, she will have $330,718.

Alex will have almost $82,000 more than Blake all because of that “minor” 1% difference in fees.

Mutual Funds vs. Index Funds Debate

I’ll let you in on a little secret because that’s what we do around here. No gatekeeping here. The mutual funds versus index funds debate is a fairly big point of contention for financial experts, especially fund managers.

They don’t want you to know HOW they are making money.

They are making money by mooching off of you. Assets under management are not transparent. In fact, it’s really hard to understand the fee structure of working with a financial advisor.

Furthermore, you might be thinking, well if I’m paying an expert to hand-pick mutual funds for me, they must be really good at their job, and I’ll get a better return on my investments.

And I wish I could tell you that were the case. Unfortunately, there is a very low chance that a fund manager will outperform a simple index fund.

In fact, a New York Times article explicitly states: “It’s very hard to beat the stock or bond market with any regularity.”

They go on with, “It found that not a single mutual fund – not one – managed to beat its benchmark in either the U.S. stock or bond markets regularly and convincingly over the last five years.”

So the reality is, even if you’re paying the 1% or 2% fee, it’s unlikely that a mutual fund will beat an index fund for long-term investors.

But for me, a financial therapist, it boils down to this:

If you are sooo uncomfortable with investing on your own that you will only invest if you have the help of a financial advisor, then investing with the help of a fund manager is better than not investing at all.

Do I think you can do it on your own? Absolutely, yes.

But if you won’t do it on your own, then *at least* do it with a fund manager.

If this is the route you take and you decide to work with a fund manager, just make sure to do these three things:

- Check that they are a fiduciary

- Negotiate the fees

And best of all, you can pay a one-time, flat-rate, hourly, or front-loaded fees. There are fee-only, not fee-based financial advisors that can help you, and will NOT charge you an AUM.

This is how Madi from Madi Manages Money does it. I would highly recommend you check her out on Nectarine, a fee-only financial advisors site.

I realize this is a How to Invest for Beginners post, and this is all getting way too nitty gritty. So I’ll jump off my soap box, and we can move on to my very favorite place to invest, Target Date Funds.

Target Date Funds

I wish I could throw confetti and blow into a kazoo here, because target date funds are worth the celebration.

Target date funds are made to be “invest it and forget it.” Here’s how it works:

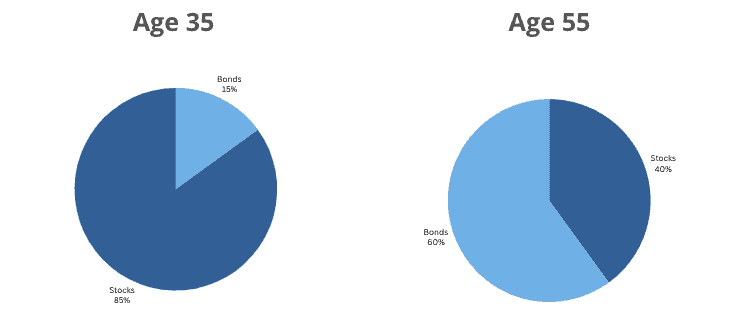

Typically, when you’re a young investor and have more time in the market, your asset allocation (how many stocks and bonds you have) leans heavier on the stocks. This is because stocks tend to have greater returns to build wealth.

Then, as you get closer to retirement age, you’ll reallocate (AKA switch around) your assets to lean heavier on bonds because they’re generally safer but have smaller returns. Target Date Funds do all the reallocating for you.

Target Date Funds Example

This is how it works:

The target date refers to the general timeline of when you want to retire.

For example, my husband is 35 and I’m 33. Let’s say we want to retire when we’re 58 and 55, respectively. So, say we want to retire in the year 2048.

The thing with Target Date funds is that they are available in increments of 5. So there’s a target date funds for 2045, 2050, 2055, 2060, 2065, and so on. That means we would choose a target date fund for the year 2050.

Just like stocks have a ticker symbol, target date funds have a letters that represent the entire fund.

Fidelity’s Freedom 2050 Fund: FFFHX

Vanguard’s Target Retirement 2050 Fund: VTTSX

When you choose a target date fund, you’re not locked into anything. You can always move your assets around and invest in different target date funds (or other index funds or whatever you want to invest in).

Target date funds are perfect for those who wants to invest, but don’t have a clue – and don’t want to have a clue – about how to do it.

They’re also great for even the savviest investors because they’re easy and work.

All in all, Target Dates Funds are the crème de la crème and my favorite way to make investing easy.

How to Invest for Beginners: Q&A

I want to address a couple questions that I often get from women who are new to investing.

“What do you do?”

The first question I always get is: What do you do?

And honestly, I’m happy to share.

We have a 401(k) from my husband’s employer, I have a small 401(k) from a previous employer (that I no longer contribute to), we each have a Roth IRA, we have a brokerage account, we have an HSA, and we have a 529 plan for each of our kids.

We invest in two things: a Target Date Fund and an index fund that follows the S&P 500, which is the top 500 publicly traded companies in America.

The fidelity index fund is: FXAIX

The Vanguard index fund is: VOO

I have no individual stocks. I don’t invest in crypto.

I keep investing as simple as possible. And it works.

“What if I need those extra funds?”

Another question I hear is: What if I need those extra funds?

We addressed this a little bit before, but it bears repeating. After five years of being vested, the contributions you’ve made to a Roth IRA are available without penalty.

So, in a dire case, you’ll have access to your own money. Again, I strongly discourage pulling your money out of any retirement account. But it’s still comforting to know it’s available, just in case.

Also, technically you can borrow against your 401(k) or take an early withdrawal from your 401(k) for a penalty of about 10%. Again, this is something I highly discourage you to do, but it is an option.

“Is investing gambling?”

Another question I get is is, “Is investing gambling?”

And I hear you on this one. Really, I do. Feeling like you your gambling or that you could lose your hard-earned dollars is scary.

But do you remember Taylor from the first example way at the beginning of this?

She was adding funds to a savings account, rather than investing her money. She only had $66,000 of purchasing power compared to Blake who had nearly 4 times the purchasing power with $250,000 in the stock market.

Taylor’s purchasing power significantly went down because of inflation. In other words, you’re already losing money by not investing.

Yes, the market can be volatile in the short-term. But we’re not short- term investors. We’re long-term investors, in it for the long haul. I can’t guarantee returns. But I can assure you that the 10.6% average return rate over the last 100 years doesn’t lie.

“Is it too late?”

Another concern I hear people say is, “I didn’t start early enough. Is it too late?”

And to them I say, unless you started investing when you were in the womb, you started too late.

Just kidding.

But when it comes to investing, it’s true that earlier is better. Believe me, I still kick myself for not knowing this stuff when I was 15, working at Plato’s Closet.

But as they say, “The best time to start investing was yesterday. The second best time is today.”

Even if you didn’t start investing as early as you could have, you should still start now. Any amount of time you can give yourself is totally worth it.

How to Invest for Beginners: Should You Start Investing?

One final thing I want to note about investing for beginners. And I’m hesitant to say this because I don’t want you to use it as an excuse to not invest ever.

But the truth is, it’s possible you’re not ready to be investing beyond the match of your 401(k).

This might be true if you have high-interest debt.

If you’re reading this post and have high-interest debt, which is anything over 7% – remember that’s the average rate of return for investing in an index fund that follows the S&P 500 – then you should get out from under that debt first.

Having credit card debt with an interest rate of 20, or even 30 percent, is going to be charging you so much interest that, mathematically, well the math ain’t mathin’.

You gotta get out of that debt.

Then, you can take the bull by the horns and start investing like a pro!

If, after all this, you feel like you need some extra nudging, contact me! Send me an email at lindsey@copingwithlindsey.com or message me @financialtherapistlindsey on Instagram. And let’s see if we should work together.

Clearly, I love this stuff. The whole point is to help you feel comfortable, confident, and competent with your money. So, let’s get you there.

I have a couple spots opening for financial therapy – where we get your money mindset right, we get you out of debt (and keep you out of debt), and yes, even get you investing.

The Wrap-Up: How to Invest for Beginners

You can build wealth for yourself. You can build generational wealth for your family. It is possible and I’m here to help you do just that.

I hope you found this post helpful. If so, please share it with a friend. And give the show a follow. It really helps expand the Financial Self-Care community!

Now go enjoy the rest of your day!